Automotive Turbocharger Market: By Turbo Type (Single-Turbo, Twin-Turbo, Twin-Scroll Turbo, Variable Geometry Turbo, Variable Twin Scroll Turbo, Wastegate, Electric Turbo); Vehicle Type (Passenger, Commercial, and Sports Car); Propulsion Type (Petrol, Diesel, CNG & LPG); Distribution Channel (OEM and Aftermarket); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: Aug-2025 | Format:| Report ID: AA1223696 | Delivery: 2 to 4 Hours

![pdf]()

![powerpoint]()

![excel]()

Market Snapshot

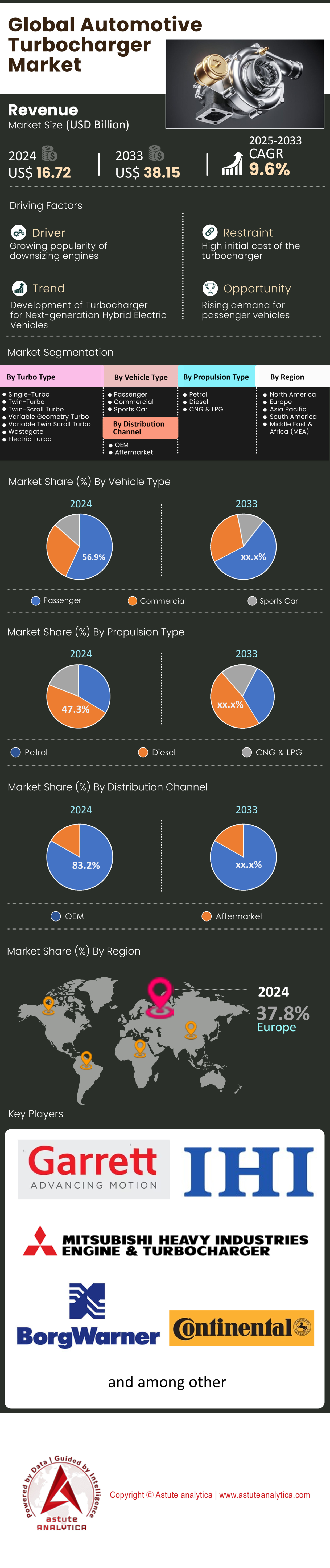

Automotive turbocharger market was valued at US$ 16.72 billion in 2024 and is projected to surpass the market valuation of US$ 38.15 billion by 2033 at a CAGR of 9.6% during the forecast period 2025–2033.

A significant demand surge in the automotive turbocharger market is being shaped by stringent new emissions regulations. The upcoming Euro 7 standard, effective from July 2025, mandates a diesel NOx limit of 60 mg/km, down from 80 mg/km previously. Furthermore, compliance longevity requirements will double to 200,000 km for cars and extend to 875,000 km for some heavy vehicles. In response, Cummins made its HE200WG turbocharger commercially available in July 2024 to meet these tough standards. Simultaneously, the anticipated draft of China 7 regulations by early 2025 is compelling manufacturers to innovate proactively.

The industry's pivot to electrification and engine downsizing is creating a strong demand for specialized turbochargers. Major players in the automotive turbocharger market are securing pivotal contracts, such as BorgWarner’s agreement for a 1.0-liter gasoline hybrid application starting production in 2027 and a separate deal for a 3.0-liter hybrid platform in 2028. Highlighting this trend, IHI Corporation’s electrically assisted turbocharger is now featured in super sports cars as of 2025. Garrett Motion is also innovating with its 3-in-1 E-Powertrain developed in 2024, which is engineered to be significantly lighter for hybrid applications.

Demand from the performance and heavy-duty sectors remains robust, driven by the need for power and efficiency. The new turbocharger on the 2024 GM L5P engine contributed to a 30-horsepower increase. In the commercial space, Cummins is launching its Holset HE400VGT in 2024, targeting the 10 to 15-liter heavy-duty truck market. The aftermarket is also expanding to meet service demand, evidenced by BORG Automotive’s February 2024 launch of 28 new turbo models covering over 1,226 unique vehicle applications. This is complemented by specialized offerings like Melett's bi-turbo kit for Mazda 2.2D models, introduced in Q2 2024.

Key Findings in Automotive Turbocharger Market

- Based on turbo type, twin-turbo segment commands a significant presence with the highest share of 26.7%

- Based on vehicle type, the passenger vehicle segment is holding the highest market share of 56.9%

- Based on propulsion type, diesel based propulsion exhibits a commanding presence with the highest share of 47.3%

- Based on distribution channel, Original Equipment Manufacturer (OEM) segment holds a dominant position in the global market, accounting for 83.2% of the total market share

- Europe is the largest market and captured over 37% market Share

- Global Automotive turbocharger market is set to surpass valuation of US$ 38.15 billion by 2033

To Get more Insights, Request A Free Sample

Three Major Shifts Shaping the Future Automotive Turbocharger Market

- Pioneering Turbochargers for Hydrogen Internal Combustion Engines (H2-ICE). A significant trend emerging in 2024 is the dedicated research and development of turbochargers for H2-ICE vehicles. Unlike gasoline or diesel, hydrogen's wide flammability range and lean-burn characteristics require a highly controlled air-management system, which the turbocharger provides. Players like Garrett Motion and BorgWarner are engineering specialized units with advanced aerodynamics and materials resistant to hydrogen embrittlement to optimize combustion, ensuring both high efficiency and power output for this next-generation zero-emission powertrain.

- The Proliferation of Variable Geometry Turbines (VGT) in Gasoline Engines. While a staple in diesel applications, VGT technology is now rapidly migrating to mass-market gasoline vehicles. This trend in the automotive turbocharger market is a direct response to the need to eliminate turbo lag and improve thermal efficiency in downsized direct-injection engines. By precisely adjusting the turbine's geometry, VGTs provide strong low-end torque and high-end power, enabling automakers to meet stringent fuel economy standards and enhance driveability without compromising on performance, a trend prominently seen in 2025 model year platforms.

- Advanced Ball Bearing Systems and Deeper Mechatronic Integration. The market is shifting from traditional journal bearings to more sophisticated dual ceramic ball bearing systems, especially in performance and hybrid applications. This reduces rotational friction by over 50%, dramatically improving transient response and spool-up time. This mechanical evolution is paired with deeper mechatronic integration, where turbochargers act as "smart" devices. They now incorporate a suite of integrated sensors for speed, temperature, and pressure, feeding real-time data to the ECU for more precise electronic boost control and predictive diagnostics.

Global Regulations Fuel Demand for Downsized Turbocharged Engines

The primary driver for automotive turbocharger market demand in mainstream global vehicles is the relentless legislative push for lower emissions and higher fuel economy. In 2024, automakers are deploying a new generation of small, potent turbo engines to meet these targets. Stellantis is rolling out its new 1.2-liter PureTech Turbo engine, which incorporates a 48V hybrid system and produces a healthy 136 horsepower. Similarly, the Volkswagen Group’s advanced 1.5L TSI evo2 engine, being deployed in 2024, is engineered for outputs of up to 268 horsepower.

Chinese automakers are at the forefront of this trend. BYD’s 2024 DM-i 5.0 hybrid system is paired with a highly efficient 1.5L engine that produces 74 kW of power, enabling some vehicle models to achieve a remarkable combined range of 2,100 kilometers. Geely’s new Thor 1.5T four-cylinder engine for its 2025 models produces 181 horsepower, while the 2025 Chery Tiggo 9 will feature a 2.0-liter turbocharged engine delivering 261 horsepower. This trend is not limited to Asia: the 2024 Hyundai Kona features a 1.6-liter turbocharged engine that generates 190 horsepower. Even as engines downsize, turbocharging is also used to "right-size" larger engines, as seen in Mazda's 2024 CX-90, whose new 3.3-liter inline-six turbo engine comes in a standard 280-horsepower version and a high-output 340-horsepower variant. A classic example is the 2025 MINI Cooper S, which uses a 2.0-liter turbocharged engine to make 201 horsepower.

Electrified Performance Turbocharging Creates a New Premium Power Frontier

At the high end of the global automotive turbocharger market, a technological revolution is underway as turbocharging merges with electrification to deliver unprecedented performance. The 2025 Porsche 911 Carrera GTS is a prime example, debuting a T-Hybrid system with a new 3.6-liter engine. At its heart is an innovative electric turbocharger featuring an integrated 11 kW electric motor. This system provides an "overboost" function that adds 40 horsepower for up to 10 seconds, contributing to a total system output of 532 horsepower. Rival German automaker BMW is set to release its 2025 M5 hybrid, which is projected to have a staggering total output of 718 horsepower. Its twin-turbo 4.4-liter V8 engine is rated at an impressive 577 horsepower on its own. This trend is echoed by British and Italian supercar manufacturers. The 2025 McLaren Artura features a 3.0-liter twin-turbo V6 producing 596 horsepower before electric assistance.

Ferrari has pushed the boundaries even further with its 296 platform; its V6 engine produces an immense 654 horsepower from combustion alone. This achievement results in a record-breaking specific output of 218 horsepower per liter, a testament to advanced turbocharging engineering. Further showcasing the extreme power of these systems, the 2025 Mercedes-AMG GT 63 S E PERFORMANCE uses its twin-turbo V8 and electric motor to generate a total system torque of 1,420 Nm.

Segmental Analysis

Twin-Turbo Systems Command the High-Performance Automotive Turbocharger Market

The twin-turbo configuration asserts its dominance in the high-performance segment of the global market, pushing engine output to new heights. For 2024 and 2025, powerful vehicles rely on this technology. The 2024 BMW M2 uses a twin-turbo inline-six for 453 horsepower, while Audi’s RS5 gets 444 horsepower from its twin-turbo V6. Porsche has widely integrated this technology; its Panamera Turbo E-Hybrid uses a twin-turbo V8, and the Cayenne Turbo E-Hybrid achieves a staggering 729 horsepower. This trend extends to luxury SUVs, with the 2025 Lexus LX using a 409-horsepower twin-turbo V6. This adoption solidifies the twin-turbo's position as the premier solution for manufacturers seeking maximum power. The innovation in the automotive turbocharger market is further shown by the 2025 Ram's new engine, which uses advanced turbo tech to deliver a massive 1,075 lb-ft of torque.

- The 2025 Lexus GX model is equipped with a powerful 349-horsepower twin-turbo V6 engine, highlighting its application in premium off-road vehicles.

- Dodge's upcoming 2026 Charger Scat Pack features a SIXPACK engine with twin turbos reaching a peak boost of 30 psi.

- The all-electric Renault 5 Turbo 3E, launched in 2024, creatively uses the "turbo" name while its two electric motors deliver immense instant torque.

The preference for twin-turbo systems in the performance sector is a defining feature of the current automotive turbocharger market. Automakers consistently choose this technology for their flagship models, from sports sedans to luxury SUVs. Data from 2024 and 2025 models indicates this is a long-term strategic direction. As brands like Porsche and BMW showcase the capabilities of twin-turbocharging, it reinforces the technology's premium status. This widespread implementation underscores the innovative drive within the performance segment of the global market. The evolution of these systems is a critical area to watch, as they are central to the strategy of leading automakers. This sustained demand indicates the robust nature of this specialized market, where power remains a paramount consumer demand.

Passenger Vehicles Spearhead Volume Growth in the Automotive Turbocharger Market

The passenger vehicle segment is the undeniable engine of growth for the global market, holding the largest share due to widespread adoption. For 2024, mainstream models like the Ford Mustang come standard with a turbocharged 2.3-liter EcoBoost. The technology is no longer a niche feature; the Honda Civic Si offers 200 horsepower from a 1.5-liter turbo, and the Kia K5 GT-Line delivers 180 horsepower. Performance compacts like the Hyundai i30 Sedan N deliver 206kW of power. Luxury brands have also made turbocharging a cornerstone, with the 2024 Mercedes-AMG C43 generating 402 horsepower and the base Porsche Cayenne using a 349-horsepower turbo V6. The sheer volume of cars like the 2025 Kia K4 featuring a turbo engine in popular trims highlights the technology’s integral role in the modern automotive turbocharger market.

- The 2024 Dodge Hornet R/T showcases turbo integration in plug-in hybrids, delivering a combined 288 horsepower.

- A standard passenger car turbocharger is engineered to last approximately 150,000 miles, aligning with vehicle lifespan expectations.

- Automakers are building new platforms around this technology, with the 2025 Mazda CX-70 offering two 3.3-liter turbocharged inline-six engine options.

This deep penetration into the passenger sector is fundamental to the sustained expansion of the global automotive turbocharger market. Engine downsizing—using smaller turbo engines to replace larger ones for better fuel economy—is now standard practice. This trend is a primary driver of demand. From compact cars to luxury SUVs and hybrids, the turbocharger has become essential for meeting both emissions regulations and consumer performance expectations. The continued innovation and application in such a high-volume segment signal a healthy and expanding future. As this trend persists, the growth trajectory for the market remains strong, anchored by the world's largest vehicle segment.

Diesel Propulsion Relies Heavily on Advanced Automotive Turbocharger Technology

Diesel engines, particularly in commercial sectors, hold a commanding presence in the global automotive turbocharger market, driven by the need for high torque and efficiency. Modern diesel engines are almost exclusively turbocharged. For 2025, manufacturers are introducing more advanced systems. Ram's new 6.7-liter Cummins turbodiesel produces a remarkable 1,075 lb-ft of torque through sophisticated turbo technology. Similarly, Volvo's new D13 Variable Geometry Turbo (VGT) engine offers up to 1,850 pound-feet of torque, showing the critical role of VGTs in the market. The durability of these systems is also key; a turbo on a diesel truck lasts 150,000 to 200,000 miles, while in power generation, it can run for 50,000 hours. This highlights their robustness and the strength of the diesel segment.

- Isuzu will launch a new 2.2-litre turbo-diesel in its 2025 D-Max, producing 120kW and 400Nm of torque.

- Stock diesel truck engines frequently operate at boost pressures around 30 PSI, much higher than gasoline counterparts.

- In the maritime sector, turbochargers are essential, capable of increasing a large diesel engine's power output by 30-40%.

The symbiotic relationship between diesel engines and turbochargers ensures this segment's dominance within the global automotive turbocharger market. For commercial operations like trucking and marine transport, no alternative offers the same power, economy, and reliability. Stricter emissions rules are pushing innovation, leading to more efficient designs like VGTs. Investments by Cummins and Volvo in new diesel turbo platforms for 2025 and beyond confirm a long-term commitment. This sustained focus guarantees the diesel segment will remain a vital and profitable part of the overall market for the foreseeable future, anchoring the industry with its consistent, high-value demand.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

OEMs Drive the Global Automotive Turbocharger Market Through Strategic Integration

The Original Equipment Manufacturer (OEM) channel is the cornerstone of the global market, reflecting the deep integration of turbocharging at the factory level. Suppliers thrive on long-term contracts. BorgWarner's 18-year partnership with a major East Asian OEM was recently extended with a 2025 contract for hybrid SUV turbos. Further cementing its leadership, BorgWarner secured deals for 1.0-liter engines in Europe (starting 2027) and high-performance units for 3.0-liter hybrids in North America (starting 2028). Stellantis echoed this by extending its Cummins partnership through 2030, putting the 6.7L Turbo Diesel in 2025 Ram trucks. The scale is massive, with facilities like BorgWarner's Mexico plant producing 3 million turbochargers annually. This factory-fit strategy is the primary driver shaping the automotive turbocharger market.

- Volvo Trucks North America has made its new D13 VGT engine standard on its second-generation VNR regional haul tractor.

- Commercial production of Volvo's D13 VGT engine began in October 2024, with CARB-compliant versions slated for late 2025.

- Production for BorgWarner's hybrid SUV contract will be at its Pyongtaek plant in Korea, starting in 2027 for supply chain efficiency.

The overwhelming dominance of the OEM segment defines the global automotive turbocharger market. Automakers engage in deep collaborations to develop and integrate bespoke turbocharging solutions fundamental to their powertrain strategies. These partnerships are essential for meeting complex targets for performance, efficiency, and emissions. The trend of localizing production, as seen with BorgWarner's plants in Mexico and Korea, strengthens these OEM relationships by improving supply chain reliability. As long as internal combustion and hybrid engines are produced, the OEM channel will remain the primary force shaping the technology, volume, and revenue of the market. This makes it a stable and predictable sector where health is directly tied to foundational OEM partnerships.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Europe: Turbo Hybridization Drives Compliance and Performance

Currently, Europe is controlling the dominating 37% market share in the automotive turbocharger market. European demand for turbochargers is overwhelmingly shaped by emissions compliance and the adoption of hybrid technology. The new Opel Frontera, launching in 2025, exemplifies this with its 1.2-liter turbo engine developed specifically for hybrid use, offered in a 100-horsepower version and a more potent 136-horsepower setup. The higher-output variant is paired with a 21-kW electric motor. Renault’s 2025 lineup features a new 1.2L mild-hybrid turbo engine delivering 96 kW of power and 230 Nm of torque. For larger vehicles, the 2024 Skoda Superb utilizes a powerful 2.0L TSI engine available in both a 204-horsepower configuration and a top-tier 265-horsepower all-wheel-drive version that produces 400 Nm of torque.

The performance segment is also embracing advanced turbocharging. The 2025 BMW X3 M50, built in Spartanburg but specified for Europe, features a 3.0-liter inline-six turbo with a 48-volt mild-hybrid system, delivering a robust 375 horsepower and 540 Nm of torque for the European market. BorgWarner is supporting this regional production push from its plant in Rzeszów, Poland, which has an annual capacity to produce over 1 million turbochargers. To meet the service needs of this growing and complex vehicle fleet, UK-based aftermarket specialist Melett continues to expand its catalog, introducing more than 160 new turbocharger components in the first half of 2024 alone.

Asia Pacific: Turbocharged Hybrids Redefine the Mainstream Market

The Asia Pacific region, led by China, is a hotbed for automotive turbocharger market, driven by the rapid expansion of sophisticated plug-in hybrid electric vehicles (PHEVs). For 2024, Great Wall Motors upgraded its Tank 400 Hi4-T, pairing a 2.0L Miller cycle turbo engine producing 185 kW of power and 380 Nm of torque with an electric motor for a combined system torque of 750 Nm. Geely’s 2024 Galaxy L7 SUV uses the Thor plug-in hybrid system with a 1.5L turbocharged engine that delivers a total system output of 390 horsepower and 535 Nm of torque. Not to be outdone, Chery’s 2025 Tiggo 9 will be equipped with a 2.0L turbo engine generating a strong 261 horsepower.

In Japan, the 2025 Subaru Forester now offers a 1.8-liter direct-injection turbo flat-four engine producing 177 horsepower and a substantial 300 Nm of torque, a significant update for the domestic market. India’s market is also seeing a turbo boom, with the 2024 Mahindra XUV 3XO featuring a 1.2L TGDi turbo-petrol engine that delivers 129 horsepower and 230 Nm of torque. Further demonstrating the region's focus on future tech, Hyundai is advancing hydrogen applications, with its N Vision 74 concept's powertrain featuring a twin-motor setup with a staggering power output of over 500 kW.

North America: High-Output Turbo Engines Power Trucks and Performance Cars

In North America automotive turbocharger market, demand is characterized by the "power and size" mantra, with turbochargers being essential for light trucks and high-performance vehicles. The 2025 Ford Explorer exemplifies this, offering a standard 2.3L EcoBoost turbo engine with 300 horsepower and 310 lb-ft of torque, and a powerful 3.0L twin-turbo V6 option that generates 400 horsepower and 415 lb-ft of torque. General Motors is also prominent, with its 2025 Chevrolet Tahoe featuring a second-generation 3.0L Duramax turbo-diesel engine that produces an impressive 495 lb-ft of torque. Stellantis will produce its new 3.0L Hurricane twin-turbo engine, with an output of up to 540 horsepower, at its Saltillo, Mexico plant.

The performance segment in the automotive turbocharger market is equally robust. The 2025 Cadillac CT5-V, a tamer version of the Blackwing, uses a 3.0L twin-turbocharged V6 that produces a formidable 360 horsepower and 405 lb-ft of torque. Its more extreme sibling, the 2025 CT5-V Blackwing, uses a 6.2L supercharged V8 to make 668 horsepower and 659 lb-ft of torque. To support this market, Cummins announced in January 2024 a massive $580 million investment in its Rocky Mount, North Carolina engine plant. This investment will upgrade assembly lines for next-generation products and create 80 new jobs, with project completion slated for 2027.

Major Capital Moves Reshaping the Global Automotive Turbocharger Market

- Cummins Announces $580 Million Investment in North Carolina Plant (January 2024): Cummins Inc. revealed a significant investment of more than $580 million across its U.S. engine manufacturing network, primarily at its Rocky Mount Engine Plant in North Carolina. The funds will be used to upgrade facilities to support the production of next-generation engines and create approximately 80 new jobs.

- Garrett Motion Completes $800 Million Senior Unsecured Notes Offering (May 2024): Garrett Motion Inc. successfully completed a private offering of $800 million in 7.750% senior unsecured notes due in 2032. The company used the proceeds to redeem its existing 5.125% senior secured notes due 2029, a move expected to generate approximately $15 million in annual cash interest savings.

- BorgWarner Acquires Eldor's Electric Hybrid Systems Business (July 2023, Finalized Early 2024): While the agreement was announced in 2023, the integration and strategic implementation of BorgWarner's acquisition of Eldor Corporation S.p.A.'s Electric Hybrid Systems business segment have been a key focus in 2024. The acquisition enhances BorgWarner’s portfolio in high-voltage hybrid technology, particularly in compact and efficient onboard chargers.

- Garrett Motion Executes $174 Million in Share Repurchases (H1 2024): In a move signalling strong confidence in its financial position, Garrett Motion repurchased $174 million of its common stock during the first half of 2024. This includes $109 million in the first quarter and an additional $65 million in the second quarter, showing the real trend in the automotive turbocharger market.

- PACCAR and Cummins Partner on Advanced Engine Development (Ongoing 2024 Investment): PACCAR, Cummins, and Daimler Truck have formed a joint venture to accelerate the development of advanced battery cells for electric commercial vehicles. While focused on EVs, this significant capital alliance allows Cummins to strategically allocate other R&D funds towards advancing its core internal combustion engine and turbocharger technologies for partners like PACCAR.

- IHI Corporation Invests in New Aero-Engine Manufacturing Facilities (Announced 2024): IHI Corporation announced investment plans for new manufacturing facilities for its aero-engine division. This large-scale investment indirectly benefits its automotive turbocharger business by advancing shared material science research (e.g., heat-resistant alloys) and high-speed rotational dynamics technology.

- Stellantis Invests in Saltillo Plant for Hurricane Engine Production (Ongoing 2024): Stellantis has made significant ongoing investments into its Saltillo, Mexico engine plant to ramp up production of the new 3.0L twin-turbo "Hurricane" engine family. This includes funding for advanced assembly lines and quality control systems for the complex turbocharging architecture used in the new Ram 1500 and other vehicles.

- Toyota Commits $1.3 Billion to Kentucky Plant for EV and Engine Production (February 2024): Toyota announced a $1.3 billion investment in its Georgetown, Kentucky facility. While a portion is for EV assembly, the investment also supports the continued production of internal combustion engines, including those equipped with turbochargers, ensuring a future supply for its popular hybrid and gasoline models.

- Hyzon Motors Secures New Capital for Hydrogen Powertrain Development (2024): Hyzon Motors, a key player in hydrogen fuel cell commercial vehicles which rely on electric air compressors (a form of turbocharging), has secured new financing and strategic agreements in 2024 to scale its production. This investment directly fuels the demand and development of specialized electric compressors for fuel cell applications.

- Komatsu Focuses Investment on Power-Agnostic Drivetrains (2024 Strategy): Komatsu, a major customer for off-highway turbochargers from suppliers like Cummins, outlined its 2024 investment strategy focusing on a power-agnostic approach. This includes R&D funding for hydrogen, electric, and advanced diesel platforms, ensuring continued investment in the robust turbocharger technologies required for the high-power-density engines used in construction and mining.

Top Players in the Automotive Turbocharger Market

- BorgWarner Inc.

- Bullseye Power Turbo Chargers

- Continental AG

- Cummins Inc.

- Garrett Motion Inc.

- HKS Co., Ltd

- Mitsubishi Heavy Industries Engine & Turbocharger

- IHI Corporation

- Magnum Performance Turbos Inc.

- Hitachi Astemo, Ltd.

- Precision Turbo and Engine

- Man Energy Solutions

- MAHLE GMBH

- Melett Ltd.

- Other Prominent Players

Market Segmentation Overview:

By Turbo Type

- Single-Turbo

- Twin-Turbo

- Twin-Scroll Turbo

- Variable Geometry Turbo

- Variable Twin Scroll Turbo

- Wastegate

- Electric Turbo

By Vehicle Type

- Passenger

- Commercial

- Sports Car

By Propulsion Type

- Petrol

- Diesel

- CNG & LPG

By Distribution Channel

- OEM

- Aftermarket

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 16.72 Billion |

| Expected Revenue in 2033 | US$ 38.15 Billion |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Bn) |

| CAGR | 9.6% |

| Segments covered | By Turbo Type, By Vehicle Type, By Propulsion Type, By Distribution Channel, By Region |

| Key Companies | BorgWarner Inc., Bullseye Power Turbo Chargers, Continental AG, Cummins Inc., Garrett Motion Inc., HKS Co., Ltd, Mitsubishi Heavy Industries Engine & Turbocharger, IHI Corporation, Magnum Performance Turbos Inc., Hitachi Astemo, Ltd., Precision Turbo and Engine, Man Energy Solutions, MAHLE GMBH, Melett Ltd., Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Choose License Type

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |